Nigeria is back in a recession for the second time in four years, no thanks to COVID-19 and the crash in oil prices triggered by the pandemic.

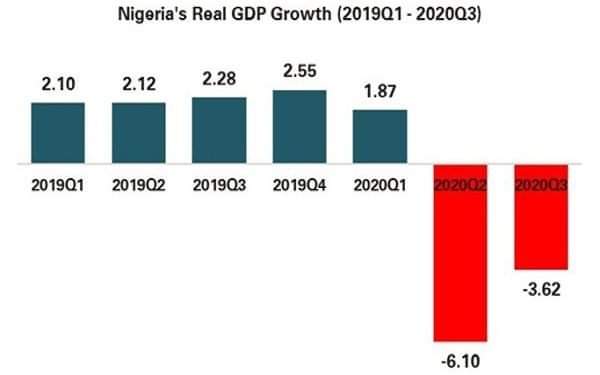

The Gross Domestic Product (GDP) contracted for the second consecutive quarter this year, recording a growth rate of -3.62 per cent (year-on-year) in the Third Quarter (Q3), according to figures published yesterday by the National Bureau of Statistics (NBS).

“Cumulative GDP for the first 9 months of 2020 therefore stood at -2.48%,” NBS Statistician General Yemi Kale, said on Twitter.

He said the oil sector contracted by 13.89% in the third quarter against growth of 6.49% in the same period a year earlier, while the non-oil sector shrunk by 2.51% in the three-months to September.

Much of the economy was on lockdown between late February and early May on account of the coronavirus pandemic.

The NBS in a report “Nigerian Gross Domestic Product Report – Q3 2020” yesterday however said the Q3 contraction was an improvement of 2.48 per cent points over the –6.10 per cent growth rate recorded in the preceding quarter (Q2 2020).

It said growth in Q3 2020 was slower by 5.90 per cent points when compared to the third quarter of 2019 which recorded a real growth rate of 2.28 per cent year on year.

“The performance of the economy in Q3 2020 reflected residual effects of the restrictions to movement and economic activity implemented across the country in early Q2 in response to the COVID-19 pandemic,” the bureau said.

As these restrictions were lifted, businesses re-opened and international travel and trading activities resumed, some economic activities have returned to positive growth.

It added: “A total of 18 economic activities recorded positive growth in Q3 2020, compared to 13 activities in Q2 2020.

“During the quarter under review, aggregate GDP stood at N39,089,460.61 million in nominal terms.

“This performance was 3.39 per cent higher when compared to the third quarter of 2019 which recorded an aggregate of N37,806,924.41 million.

“This rate was, however, lower relative to growth recorded in the third quarter of 2019 by –9.91 per cent points but higher than the preceding quarter by 6.19 per cent points.”

In the overview, the NBS said the average daily oil production recorded in the third quarter of 2020 stood at 1.67 million barrels per day (mbpd), or 0.37mbpd lower than the average production recorded in the same quarter of 2019 and 0.14mbpd lower than production volume recorded in the second quarter of 2020.

It said that the real growth for the oil sector was –13.89 per cent (year-on-year) in Q3 2020, indicating a sharp contraction of –20.38 per cent points relative to the rate recorded in the corresponding quarter of 2019. Furthermore, real oil growth decreased by –7.26 per cent points when compared with oil sector growth recorded in Q2 2020 (6.63 per cent).

NBS said quarter on quarter, however, the oil sector recorded a growth rate of 9.64 per cent in Q3 2020. The sector contributed 8.73 per cent to total real GDP in Q3 2020, down from 9.77 per cent and 8.93 per cent respectively recorded in the corresponding period of 2019 and the preceding quarter, Q2 2020.

On the non-crude oil sector, the report said “the non-oil sector grew by –2.51 per cent in real terms during the reference quarter, which is –4.36 per cent points lower than the rate recorded in Q3 2019 but 3.54 per cent points higher than in the second quarter of 2020.”

The report said the non-oil sector was driven mainly by Information and Communication (Telecommunications), with other drivers being Agriculture (Crop Production), Construction, Financial and Insurance (Financial Institutions), and Public Administration.

In real terms, according to the report, the non-oil sector contributed 91.27 per cent to the nation’s GDP in the third quarter of 2020, higher than its share in the third quarter of 2019 (90.23 per cent) and the second quarter of 2020 (91.07 per cent).

Nigeria had, earlier in 2016 slipped into recession but was able to recover in the second quarter of the following year when it posted a 0.7 per cent growth.

In June, the World Bank warned that Nigeria faced its worst recession in four decades after revising its 2020 forecast for Nigeria’s economy to -4.1 per cent from its previous projection of -3.2 per cent.

The World Bank had projected that the collapse in oil prices coupled with the COVID-19 pandemic would plunge the Nigerian economy into a severe economic recession, the worst since the 1980s.

In a report, ”Nigeria In Times of COVID-19: Laying Foundations for a Strong Recovery,” the organisation estimated that Nigeria’s economy would likely contract by 3.2% in 2020.

The projection assumed that the spread of COVID-19 in Nigeria would be contained by the third quarter of 2020.

It feared that if the spread of the virus became more severe, the economy could contract further. Before COVID-19, the Nigerian economy was expected to grow by 2.1% in 2020, which means that the pandemic has led to a reduction in growth by more than five percentage points.

Shubham Chaudhuri, World Bank Country Director for Nigeria had said at the time that: ”While the long-term economic impact of the global pandemic is uncertain, the effectiveness of the government’s response is important to determine the speed, quality, and sustainability of Nigeria’s economic recovery. Besides immediate efforts to contain the spread of COVID-19 and stimulate the economy, it will be even more urgent to address bottlenecks that hinder the productivity of the economy and job creation.”

Marco Hernandez, World Bank Lead Economist for Nigeria and co-author of the report said: ”The unprecedented crisis requires an equally unprecedented policy response from the entire Nigerian public sector, in collaboration with the private sector, to save lives, protect livelihoods, and lay the foundation for a strong economic recovery.”

Second recession not a surprise — Dons

Reacting to the development yesterday, a professor of banking and finance, Uche Uwaleke, described the third quarter GDP figures released by the NBS as “a confirmation of the fact that in terms of economic contraction occasioned by COVID’19, Q2 2020 represents the worst experience for Nigeria.”

Uwaleke, who teaches at the Nasarawa State University, told The Nation that the situation could have been worse in Q2 of 2020 but for government’s responses like “the ease in lockdowns and movement restrictions, the reduction in the cases of COVID-19 and the gradual return of investors’ confidence in the economy.”

But he asked the National Assembly to quickly pass the 2021 budget to hasten the country’s economic recovery.

He said there could be “a quick V-shaped recovery as the effect of COVID-19 recedes and the impact of the interventions by the government and CBN begins to manifest, including the implementation of the Economic Sustainability Plan.”

In his own response, a visiting professor at the Centre for the Study of Leadership and Complex Military Operations, Nigeria Defence Academy (NDA), Ken Ife, said he was “not surprised that Nigeria slipped into recession both as the aftermath of the lockdown and as part of the ongoing macroeconomic headwinds.”

He said: “The unusual type of recession we dropped into, stagflation, is one where rather than the economy experiencing low inflation, low interest rates with expansionary policies, we are just seeing the opposite in galloping inflation, high interest rates and fiscal and monetary policy challenges despite quantitative domestic finance interventions.

”At a contraction of -3.62%, there is a likelihood we might jump out of recession in the 4th Qtr of 2020, but certainly, in the 1st Qtr of 2021, all things being equal.”

Also contributing, a former Chief Economist of the Nigerian Labour Congress (NLC), Dr. Peter Ozon-Eson, attributed the recession to what he called the adverse policies of the Federal Government.

He said the hike in the pump price of petrol at a time other nations were lowering their tariffs in the face of the COVID-19 pandemic was largely responsible for the situation.

He said: “We adopted policies domestically that have further depleted the economy.

“Most countries at this period adopted policies that will at least cushion the negative effects of COVID-19, but we chose that period to inflict more hardship on the citizens.

“The aggregate demand for domestically produced goods was inflated because of the adverse policies we chose to adopt at a very wrong time.

“The cost of electricity has gone up. To add insult to injury, we also have general insecurity in the country, which has impacted negatively on agricultural production.”

A former Central Bank of Nigeria (CBN) Deputy Governor, Dr. Obadiah Mailafia, shared Ozon-Eson’s view on insecurity as a major cause of the recession.

His words: “There is uncertainty and crisis of confidence. These things are bound to undermine growth.”

He said there is hunger in the land, and once poverty is unchecked, it can result in the grave one of insecurity and a vicious circle of decline.

Proffering a solution, the economic expert said: “We have to provide a better environment that is secured and protects everyone.”

The worst may be possibly over — LCCI

The Lagos Chamber of Commerce and Industry (LCCI) says the nation’s economic contraction of 3.62 per cent of the third quarter against the 6.1 per cent of the second quarter of the year may indicate that the worst is over.

Reacting to the National Bureau of Statistics (NBS) quarterly report, LCCI Director-General, Dr Muda Yusuf, told newsmen that the news of recession was not surprising.

Yusuf said the EndSARS crisis might perpetuate the recession into the fourth quarter.

He added that the protests and the destruction that followed were major setbacks for the nation’s economic recovery prospects.

Yusuf, however, expressed hope that the economy would return to the path of growth in the first or second quarter of 2021, barring any new disruptions to the economy.

He said: “From an economic perspective, 2020 has been a very bad year; the worst in recent history.

“We are faced with the double jeopardy of a stumbling economy and spiraling inflation.

“The October inflation numbers of 14.23 per cent was the highest in 10 months, a condition which in economic parlance is characterised as stagflation.

“The effects of these developments are evident in businesses and in households.

“Regrettably, and as if these were not bad enough, the business community continues to grapple with unfavourable policy, institutional and regulatory challenges impeding investment,” he said.

The DG, however, said to facilitate quick recovery, there was need to restore normalcy to the foreign exchange market by broadening the scope of market expression in the allocation mechanism.

“The ports system, especially the key institutions in the international trade processes need to be more investment friendly.

“We should show greater commitment to the fixing of the structural issues to reduce production and operating costs for investors in the economy,” he said.

Yusuf said that following the EndSARS experience, the state of internal security had begun to impact negatively on investors’ confidence.

He noted that security presence was becoming less visible, especially in the major cities, with psychological effects which, he said, could adversely affect investment and economic recovery.

“We appreciate the setback suffered by the police as a result of the recent protests and we empathise with them.

“But we need to give security confidence to citizens and investors.

“Incidents of kidnapping, banditry, herders-farmers clashes have not abated, and these also have grave implications for investments.”

By Nduka Chiejina